Written by: Andy Himmel, Founder of The Restaurant CPAs

You’ve built something special. Your restaurants are profitable, your team is humming, and you’re starting to think about what comes next.

Maybe it’s adding three more locations. Maybe it’s catching the attention of a private equity firm. Maybe it’s just proving to yourself that this thing you’ve built has real, scalable value.

Here’s what I wish someone had told me when I was in your shoes: the metrics you obsess over every day aren’t necessarily the metrics that matter when it’s time to grow or attract capital.

I spent years focused on what I thought were the most important numbers to measure my restaurant’s success.

But I wasn’t always contextualizing those numbers in ways suitable for growth (and to catch investors’ attention).

For operators looking to strengthen their financial foundation, Restaurant CPAs connect restaurant operators with firms that specialize in restaurant bookkeeping, accounting, tax, and advisory services. Available to Beyond Broadline operators at no cost, we learn about your business and introduce you to firms with the right expertise to support stronger financial visibility and growth.

To not let history repeat itself, I sat down with John Hamburger, Founder and President of Franchise Times Corporation and Restaurant Finance Monitor, to get his take on the key financial metrics that investors actually scrutinize, and the mistakes operators make with each one.

Mistake #1: Failing to Benchmark Prime Cost Against Top Performers

Every operator knows their prime cost—the combination of food cost and labor cost. It’s on every P&L, and most can recite their numbers without looking them up.

But here’s what separates operators who attract investors from those who don’t: benchmarking.

Knowing you’re running a 62% prime cost doesn’t mean much in isolation. The real question is how that compares to the top performers in your segment. Are you in line with the best casual dining operators? Running three points higher than you should be? That gap represents real money—and real opportunity.

Investors care about benchmarking because it shows you understand your competitive position. It tells them you’re not just managing your business in a vacuum; you’re measuring yourself against the best and actively working to close the gap. That’s the kind of operational self-awareness that signals a scalable, investable brand.

But benchmarking is only valuable if you have the systems to actually move the needle. Investors also want to see technology systems like:

- Inventory management that catches variance

- Labor scheduling that responds to demand patterns

- Purchasing relationships that protect your margins

This is exactly where having the right operational infrastructure becomes a competitive advantage. When you can show investors that you’re tracking theoretical versus actual food costs, monitoring purchasing trends across locations, and leveraging data to negotiate better contracts, you’re telling a story of operational maturity—not just profitability.

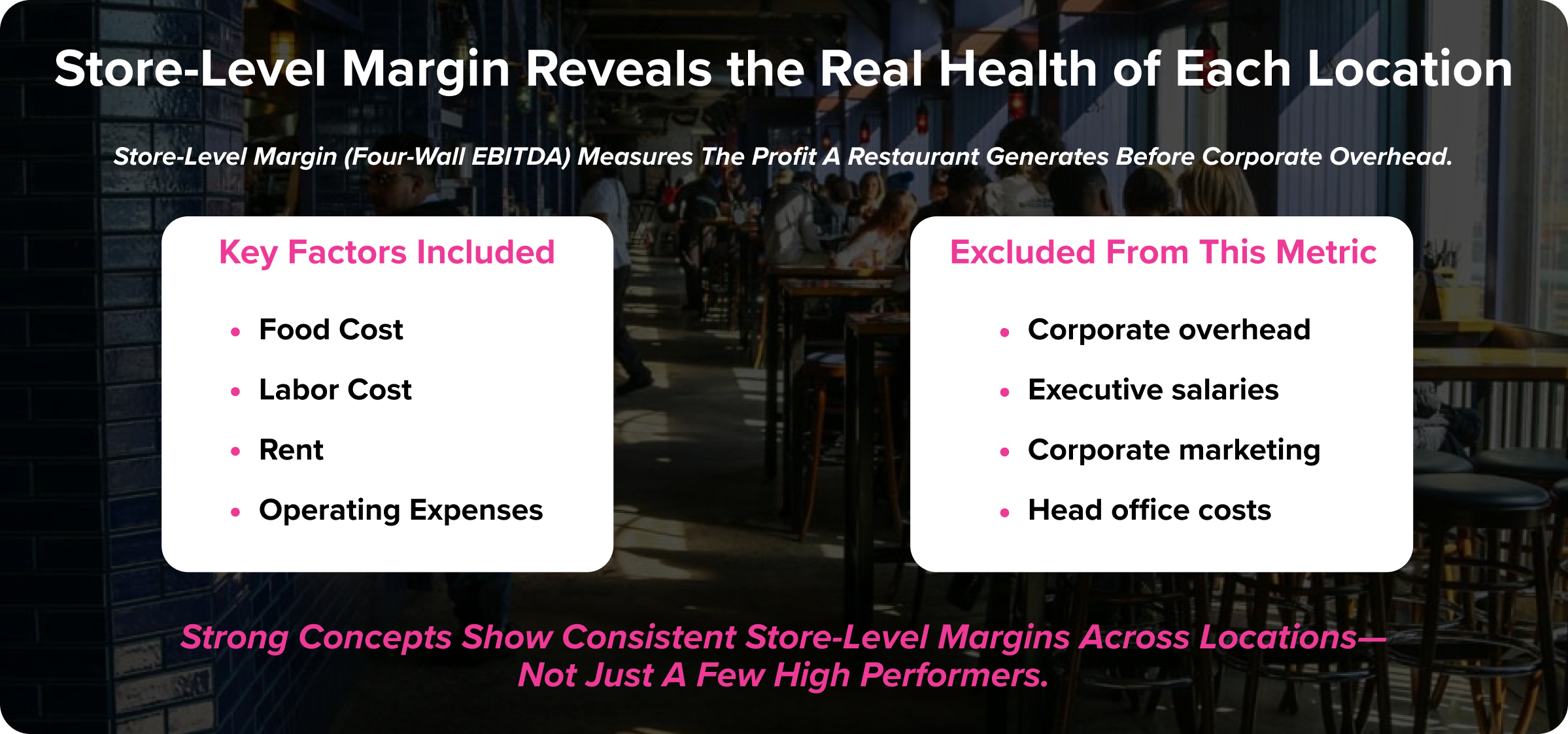

Mistake #2: Ignoring Store-Level Margin Until It’s Too Late

Store-level margin (sometimes called four-wall EBITDA or restaurant-level profit) strips away corporate overhead and tells you what each location actually contributes to the business. It’s the purest measure of whether your unit economics work.

Operators need to think hard about their four-wall economics—and focus efforts on elevating them. That means building flexible models that ebb and flow with volume, not rigid cost structures that crush you during slow periods. It also means finding ways to make your space productive for more hours of the day. Can you capture a daypart you’re currently missing? Can your labor model flex down when traffic dips and flex up when it surges?

The mistake I see operators make is conflating overall company profitability with store-level health. You can have a profitable company with underperforming stores—for a while. Maybe you’ve got three crushing it and two dragging down the average. Maybe your corporate overhead is lean enough to mask marginal unit performance.

But investors see right through this.

What they want to see is how your lower-performing stores flow through cash based on a flexible, nimble economic model—not a few star locations carrying the weight.

Sophisticated investors will peel off outliers on both the high and low ends when evaluating your business. That means the heart of your portfolio—the stores in the middle—is what really drives valuation and interest. If those core units have strong, consistent margins, you’ve got a story.

The operators who attract capital:

- Show consistent, strong store-level margins across their portfolio

- Know exactly which locations are carrying the business and which need attention.

- Articulate why new locations will perform at or above the existing average

They can do all this because they’ve done the work. They’ve optimized restaurant design, built flexible labor models, right-sized their footprint, and developed menus that balance guest appeal with operational efficiency.

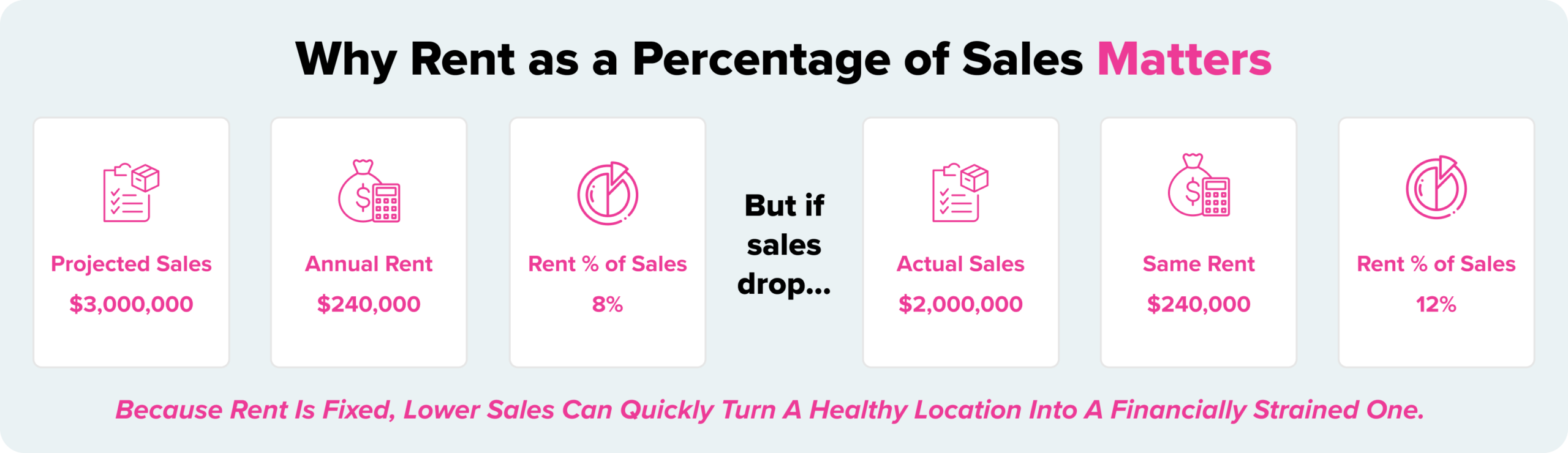

Mistake #3: Underestimating the Power of Rent as a Percentage of Sales

If there’s one metric that operators consistently underweight in their thinking, it’s rent as a percentage of sales.

John says:

“Operators tend to be too optimistic when it comes to new locations. They badly want to open a new store and will often justify the sales volume to meet the rents.”

Here’s the problem: rent is (usually) fixed. Sales are not.

Say you’re building off some strong locations and decide to go bigger—a larger footprint in a top-tier real estate site with premium rent. You project $3 million in annual sales, which puts rent at a comfortable 8%. But the market takes longer to build than expected, or it’s just not quite what you thought it was. You end up doing $2 million, and suddenly, rent is 12% of sales.

That changes everything.

Do that a few times in a tight time window, and your unit economics become a major red flag. What looked like ambitious growth now looks like a pattern of bad assumptions—and investors will see it immediately.

John shared a cautionary example:

“When you are building new locations, you can’t afford many situations where your rent as a percentage of sales is too high. If you are looking for a valuation that is predicated on opening new stores, high rent and low volumes is a business killer.”

The lesson isn’t to avoid ambitious real estate. It’s to be brutally honest about your assumptions.

As my restaurants matured, I became obsessive about this. The last two locations I did, we had strict criteria: 3,900 square feet or less, walk-in cooler on the outside (not eating up rentable square footage), and specific deal terms that protected our downside, lowering our breakeven. Because of that, those locations made money during the slow times and made a lot of money during the busy times.

Investors love seeing this kind of discipline because you’re signaling that you understand the development risk in scaling a restaurant concept.

Mistake #4: Misunderstanding How Debt Affects Your Options

Debt isn’t “good” or “bad” for restaurant operators. It all depends on how you use it.

A lot of people put debt on a business because they don’t want to put more equity into it. And in moderation, this can be a strong plan.

Sometimes you can get a better return on your capital by strategically leveraging debt.

But you don’t want to take that logic too far.

John says,

“If you were to underwrite a restaurant chain using pretty conservative metrics, you’d put maybe two times your EBITDA in debt on the business instead of five or six.”

For operators thinking about bringing in investors or positioning for a transaction, this matters enormously. Coming to the table with a clean balance sheet—or at least manageable debt levels—opens up options. Coming with a heavily leveraged business limits what investors can do and how they think about valuation.

The operators who get in trouble are the ones who take on debt to fund expansion without being conservative about their projections. They assume every new store will hit plan. They assume same-store sales will keep growing. They assume they can service the debt and still have cash flow for reinvestment.

And when those assumptions don’t hold, they’re stuck.

Build Your Restaurant’s Financial Foundation

Looking back at my own journey as an operator, I wish I’d understood these metrics earlier. Not just the numbers themselves, but the systems and discipline required to optimize them.

As I’ve learned, the operators who attract capital, get the attention of sophisticated investors, and position their businesses for premium valuations are running restaurants with better financial infrastructure than their competitors.

They understand their unit economics cold. They can explain the assumptions behind their growth projections. They have systems in place to track, monitor, and improve the metrics that matter.

That’s why the smartest operators invest in infrastructure early. They partner with procurement platforms that give them spend visibility and cost control across their supply chain. They work with specialized restaurant accountants who understand unit economics and can structure financials for growth. They build the systems that generate the metrics investors want to see—long before those investors are in the room.

Because when you’re ready for that conversation with investors, you want to be talking about the right numbers—the ones that actually matter.

Conclusion

Building a restaurant brand that attracts capital takes more than strong sales. It requires the financial discipline, operational systems, and data visibility that allow you to measure performance, benchmark against the best, and scale with confidence.

For operators looking to strengthen their financial foundation, The Restaurant CPAs provides accounting and advisory services built specifically for the restaurant industry, helping brands understand their unit economics and prepare for growth. Combined with Buyers Edge Platform’s procurement technology, supply chain insights, and purchasing visibility, operators gain the financial and operational data needed to strengthen margins and build scalable restaurant businesses.

Buyers Edge Platform brings together technology, procurement solutions, and industry expertise to help operators strengthen margins, improve unit economics, and build scalable restaurant businesses.

When the time comes to grow, expand, or attract investors, those systems make all the difference.